5.2 Solutions

5.2.1 Exercise

This question relates to the College dataset from the ISLR package.

- Split the data into a training set and a test set. Using out-of-state tuition as the response and the other variables as the predictors, perform forward stepwise selection on the training set in order to identify a satisfactory model that uses just a subset of the predictors.

library(ISLR)

library(leaps)

library(gam)

library(gbm)

library(glmnet)

library(randomForest)set.seed(12345)

train <- sample(nrow(College) * 0.7)

train_set <- College[train, ]

test_set <- College[-train, ]forward_subset <- regsubsets(Outstate ~ ., data = train_set, nvmax = ncol(College)-1, method = "forward")

model_summary <- summary(forward_subset)

plot_metric <- function(metric, yaxis_label, reverse = FALSE) {

plot(metric, xlab = "Number of Variables", ylab = yaxis_label, xaxt = "n", type = "l")

axis(side = 1, at = 1:length(metric))

if (reverse) {

metric_1se <- max(metric) - (sd(metric) / sqrt(length(metric)))

min_subset <- which(metric > metric_1se)

} else {

metric_1se <- min(metric) + (sd(metric) / sqrt(length(metric)))

min_subset <- which(metric < metric_1se)

}

abline(h = metric_1se, col = "red", lty = 2)

abline(v = min_subset[1], col = "green", lty = 2)

}

par(mfrow=c(1, 3))

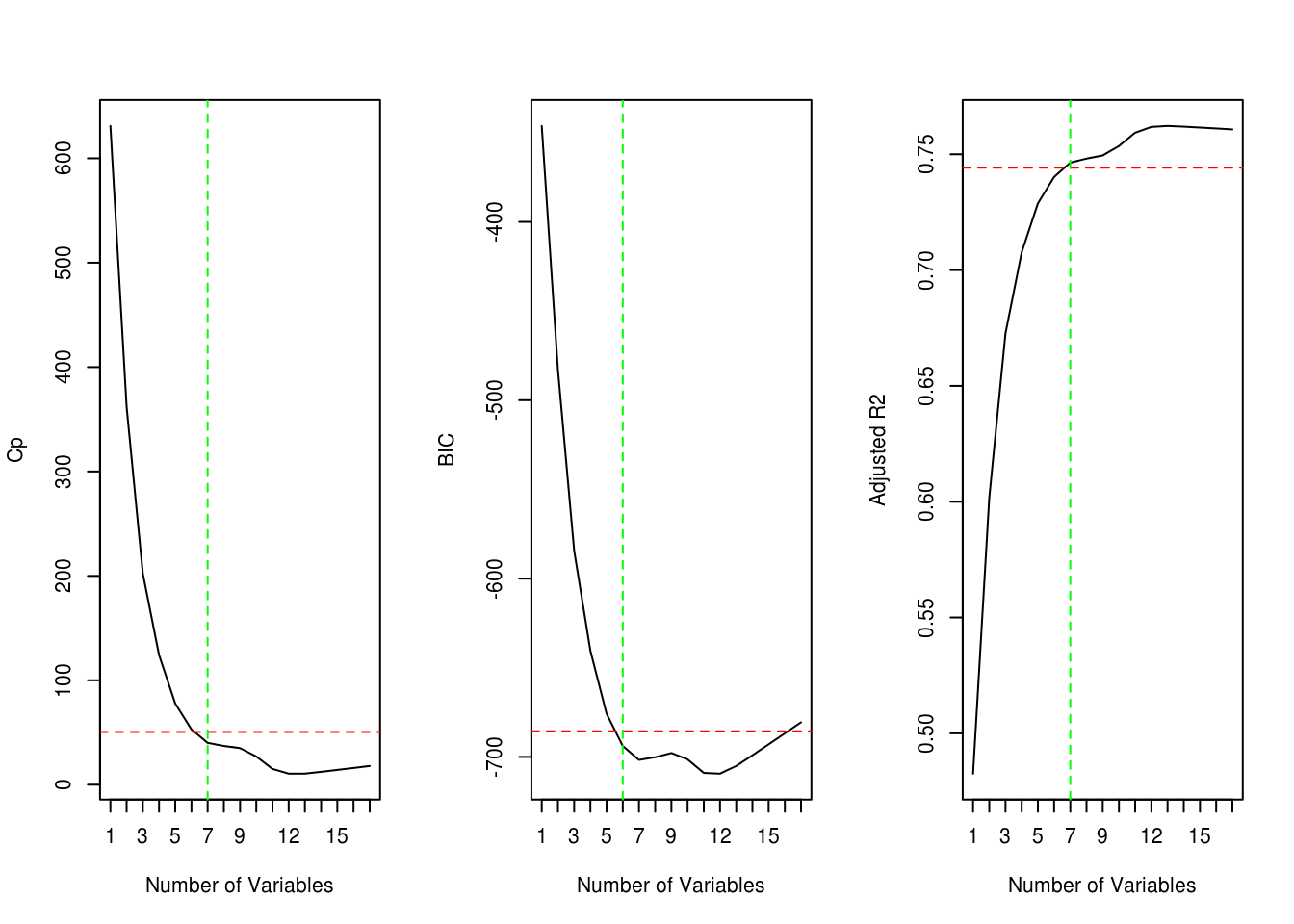

plot_metric(model_summary$cp, "Cp")

plot_metric(model_summary$bic, "BIC")

plot_metric(model_summary$adjr2, "Adjusted R2", reverse = TRUE) # higher values are better

The red dotted line shows the best metric (Cp, BIC, Adjusted R2) within 1 standard error. The green dotted line shows the subset for best metric with the smallest number of variables. Cp and Adjusted R2 give us a subset with 7 variables and BIC gives us 6.

coef(forward_subset, 6) (Intercept) PrivateYes Room.Board PhD perc.alumni

-3769.0587788 2748.6944010 0.8999634 38.5143460 44.4889713

Expend Grad.Rate

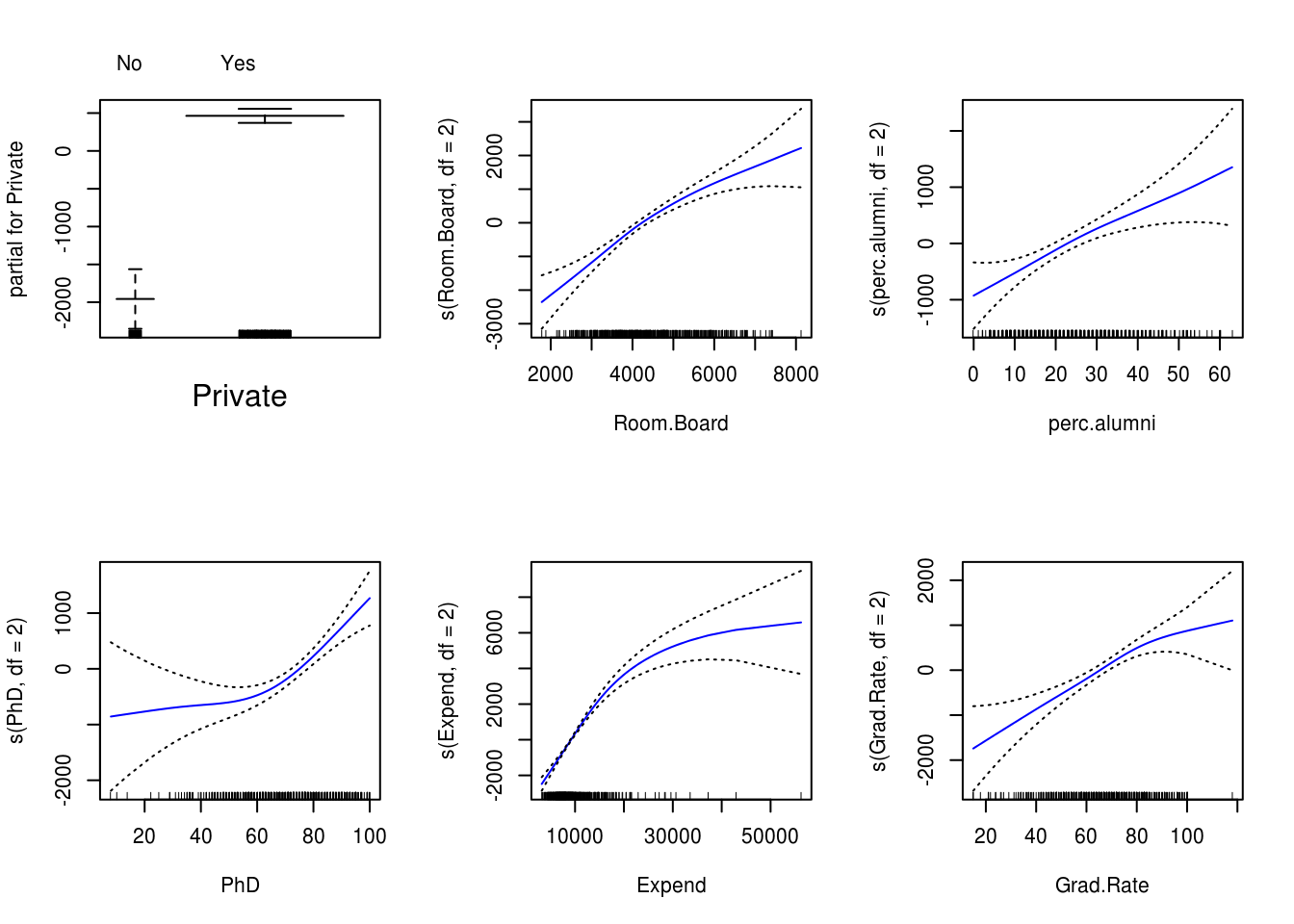

0.2543900 31.2043096 - Fit a GAM on the training data, using out-of-state tuition as the response and the features selected in the previous step as the predictors. Plot the results, and explain your findings.

gam_model <- gam(Outstate ~ Private + s(Room.Board, df=2) + s(perc.alumni, df=2) +

s(PhD, df=2) + s(Expend, df=2) + s(Grad.Rate, df=2), data=train_set)

par(mfrow=c(2, 3))

plot(gam_model, se=TRUE, col="blue")

- Evaluate the model obtained on the test set, and explain the results obtained.

Re-use some functions for calculating RMSE and R^2 from last week:

calc_mse <- function(y, y_hat) {

return(mean((y - y_hat)^2))

}

calc_rmse <- function(y, y_hat) {

return(sqrt(calc_mse(y, y_hat)))

}

calc_r2 <- function(y, y_hat) {

y_bar <- mean(y)

rss <- sum((y - y_hat)^2)

tss <- sum((y - y_bar)^2)

return(1 - (rss / tss))

}gam_predictions <- predict(gam_model, test_set)

gam_rmse <- calc_rmse(test_set$Outstate, gam_predictions)

cat("RMSE:", gam_rmse, "\n")RMSE: 1984.385 gam_r2 <- calc_r2(test_set$Outstate, gam_predictions)

cat(" R^2:", gam_r2, "\n") R^2: 0.7614328 We obtain a test RMSE of 1984.3845506 and R-squared of 0.7614328 using GAM with 6 predictors

- For which variables, if any, is there evidence of a non-linear relationship with the response?

summary(gam_model)

Call: gam(formula = Outstate ~ Private + s(Room.Board, df = 2) + s(perc.alumni,

df = 2) + s(PhD, df = 2) + s(Expend, df = 2) + s(Grad.Rate,

df = 2), data = train_set)

Deviance Residuals:

Min 1Q Median 3Q Max

-7164.185 -1192.389 9.746 1195.918 8668.434

(Dispersion Parameter for gaussian family taken to be 3515849)

Null Deviance: 8614032615 on 542 degrees of freedom

Residual Deviance: 1866916246 on 531.0002 degrees of freedom

AIC: 9739.358

Number of Local Scoring Iterations: 2

Anova for Parametric Effects

Df Sum Sq Mean Sq F value Pr(>F)

Private 1 1968096326 1968096326 559.778 < 2.2e-16 ***

s(Room.Board, df = 2) 1 1852547004 1852547004 526.913 < 2.2e-16 ***

s(perc.alumni, df = 2) 1 739433651 739433651 210.314 < 2.2e-16 ***

s(PhD, df = 2) 1 408910513 408910513 116.305 < 2.2e-16 ***

s(Expend, df = 2) 1 669471699 669471699 190.415 < 2.2e-16 ***

s(Grad.Rate, df = 2) 1 105813593 105813593 30.096 6.372e-08 ***

Residuals 531 1866916246 3515849

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Anova for Nonparametric Effects

Npar Df Npar F Pr(F)

(Intercept)

Private

s(Room.Board, df = 2) 1 5.624 0.0180708 *

s(perc.alumni, df = 2) 1 0.517 0.4725226

s(PhD, df = 2) 1 11.780 0.0006455 ***

s(Expend, df = 2) 1 70.804 4.441e-16 ***

s(Grad.Rate, df = 2) 1 3.159 0.0761031 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1Non-parametric Anova test shows a strong evidence of non-linear relationship between response and Expend and PhD, and a moderately strong non-linear relationship between response and Room.Board and Grad.Rate.

5.2.2 Exercise

Apply boosting, bagging, and random forests to a data set of your choice. Be sure to fit the models on a training set and to evaluate their performance on a test set. How accurate are the results compared to simple methods like linear or logistic regression? Which of these approaches yields the best performance?

data(Weekly)

Weekly$Direction <- Weekly$Direction == "Up"

Weekly <- subset(Weekly, select = -c(Year, Today)) # drop Year and Today columns

set.seed(12345)

train <- sample(nrow(Weekly) * 0.7)

train_set <- Weekly[train, ]

test_set <- Weekly[-train, ]# show confusion matrix from predicted class and observed class

show_model_performance <- function(predicted_status, observed_status) {

confusion_matrix <- table(predicted_status,

observed_status,

dnn = c("Predicted Status", "Observed Status"))

print(confusion_matrix)

error_rate <- mean(predicted_status != observed_status)

cat("\n") # \n means newline so it just prints a blank line

cat(" Error Rate:", 100 * error_rate, "%\n")

cat("Correctly Predicted:", 100 * (1-error_rate), "%\n")

cat("False Positive Rate:", 100 * confusion_matrix[2,1] / sum(confusion_matrix[,1]), "%\n")

cat("False Negative Rate:", 100 * confusion_matrix[1,2] / sum(confusion_matrix[,2]), "%\n")

}Logistic regression

logit_model <- glm(Direction ~ ., data = Weekly, family = binomial, subset = train)

predicted_direction <- predict(logit_model, test_set, type="response") > 0.5

show_model_performance(predicted_direction, test_set$Direction) Observed Status

Predicted Status FALSE TRUE

FALSE 128 157

TRUE 18 24

Error Rate: 53.51682 %

Correctly Predicted: 46.48318 %

False Positive Rate: 12.32877 %

False Negative Rate: 86.74033 %Boosting

boost_model <- gbm(Direction ~ ., data = train_set, n.trees=5000, distribution = "bernoulli")

predicted_direction <- predict(boost_model, test_set, n.trees=5000) > 0.5

show_model_performance(predicted_direction, test_set$Direction) Observed Status

Predicted Status FALSE TRUE

FALSE 116 143

TRUE 30 38

Error Rate: 52.9052 %

Correctly Predicted: 47.0948 %

False Positive Rate: 20.54795 %

False Negative Rate: 79.00552 %Bagging

Weekly$Direction <- as.factor(Weekly$Direction)

bag_model <- randomForest(Direction ~ ., data=Weekly, subset=train, mtry=ncol(Weekly)-1)

predicted_direction <- predict(bag_model, test_set)

show_model_performance(predicted_direction, test_set$Direction) Observed Status

Predicted Status FALSE TRUE

FALSE 18 23

TRUE 128 158

Error Rate: 46.17737 %

Correctly Predicted: 53.82263 %

False Positive Rate: 87.67123 %

False Negative Rate: 12.70718 %Random Forests

rf_model <- randomForest(Direction ~ ., data=Weekly, subset=train, mtry=2)

predicted_direction <- predict(rf_model, test_set)

show_model_performance(predicted_direction, test_set$Direction) Observed Status

Predicted Status FALSE TRUE

FALSE 21 25

TRUE 125 156

Error Rate: 45.87156 %

Correctly Predicted: 54.12844 %

False Positive Rate: 85.61644 %

False Negative Rate: 13.81215 %5.2.3 Exercise

We now use boosting to predict Salary in the Hitters dataset, which is part of the ISLR package.

- Remove the observations for whom the salary information is unknown, and then log-transform the salaries.

sum(is.na(Hitters$Salary))[1] 59Hitters <- Hitters[-which(is.na(Hitters$Salary)), ]

sum(is.na(Hitters$Salary))[1] 0Hitters$Salary <- log(Hitters$Salary)- Create a training set consisting of the first 200 observations, and a test set consisting of the remaining observations.

train <- 1:200

train_set <- Hitters[train, ]

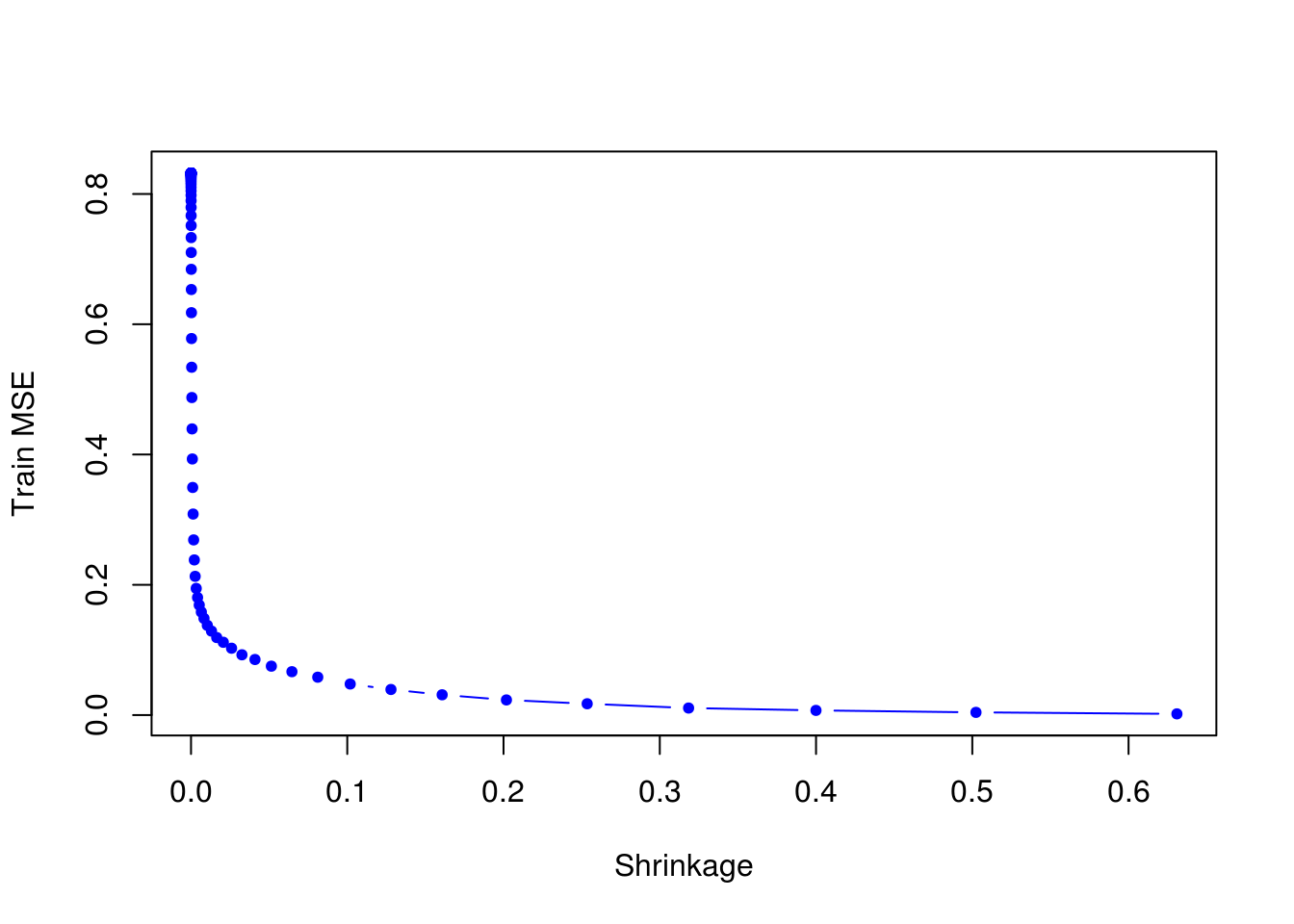

test_set <- Hitters[-train, ]- Perform boosting on the training set with 1,000 trees for a range of values of the shrinkage parameter \(\lambda\). Produce a plot with different shrinkage values on the \(x\)-axis and the corresponding training set MSE on the \(y\)-axis.

set.seed(12345)

lambdas <- 10 ^ seq(-10, -0.2, length = 100)

train_errors <- rep(NA, length(lambdas))

test_errors <- rep(NA, length(lambdas))

for (i in 1:length(lambdas)) {

boost_model <- gbm(Salary ~ . , data = train_set, distribution = "gaussian",

n.trees = 1000, shrinkage = lambdas[i])

train_predictions <- predict(boost_model, train_set, n.trees = 1000)

train_errors[i] <- calc_mse(train_set$Salary, train_predictions)

test_predictions <- predict(boost_model, test_set, n.trees = 1000)

test_errors[i] <- calc_mse(test_set$Salary, test_predictions)

}

plot(lambdas, train_errors, xlab = "Shrinkage", ylab = "Train MSE", col = "blue", type = "b", pch = 20)

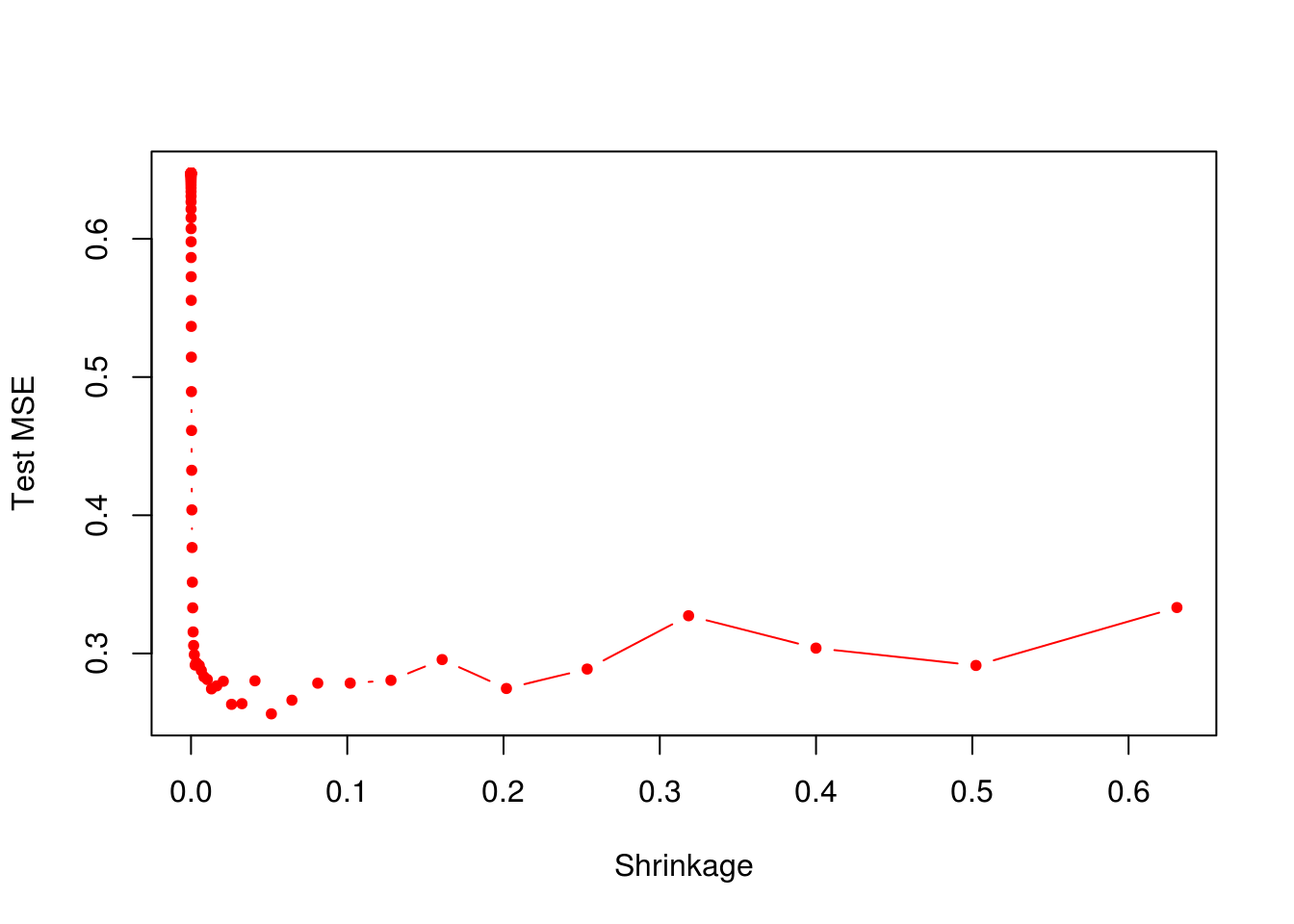

- Produce a plot with different shrinkage values on the \(x\)-axis and the corresponding test set MSE on the \(y\)-axis.

plot(lambdas, test_errors, xlab = "Shrinkage", ylab = "Test MSE", col = "red", type = "b", pch = 20)

min(test_errors)[1] 0.256307boost_lambda_min <- lambdas[which.min(test_errors)]

boost_lambda_min[1] 0.05141752Minimum test error is obtained at \(\lambda = 0.0514175\).

- Compare the test MSE of boosting to the test MSE that results from applying two of the regression approaches seen in our discussions of regression models.

OLS

ols_model <- lm(Salary ~ . , data = train_set)

ols_predictions <- predict(ols_model, test_set)

calc_mse(test_set$Salary, ols_predictions)[1] 0.4917959Lasso

set.seed(12345)

train_matrix <- model.matrix(Salary ~ . , data = train_set)

test_matrix <- model.matrix(Salary ~ . , data = test_set)

lasso_model <- glmnet(train_matrix, train_set$Salary, alpha = 1)

lasso_predictions <- predict(lasso_model, s=0.01, newx=test_matrix)

calc_mse(test_set$Salary, lasso_predictions)[1] 0.4700537Both linear model and regularization like Lasso have higher test MSE than boosting.

- Which variables appear to be the most important predictors in the boosted model?

boost_model <- gbm(Salary ~ . , data = train_set, distribution="gaussian",

n.trees = 1000, shrinkage = boost_lambda_min)

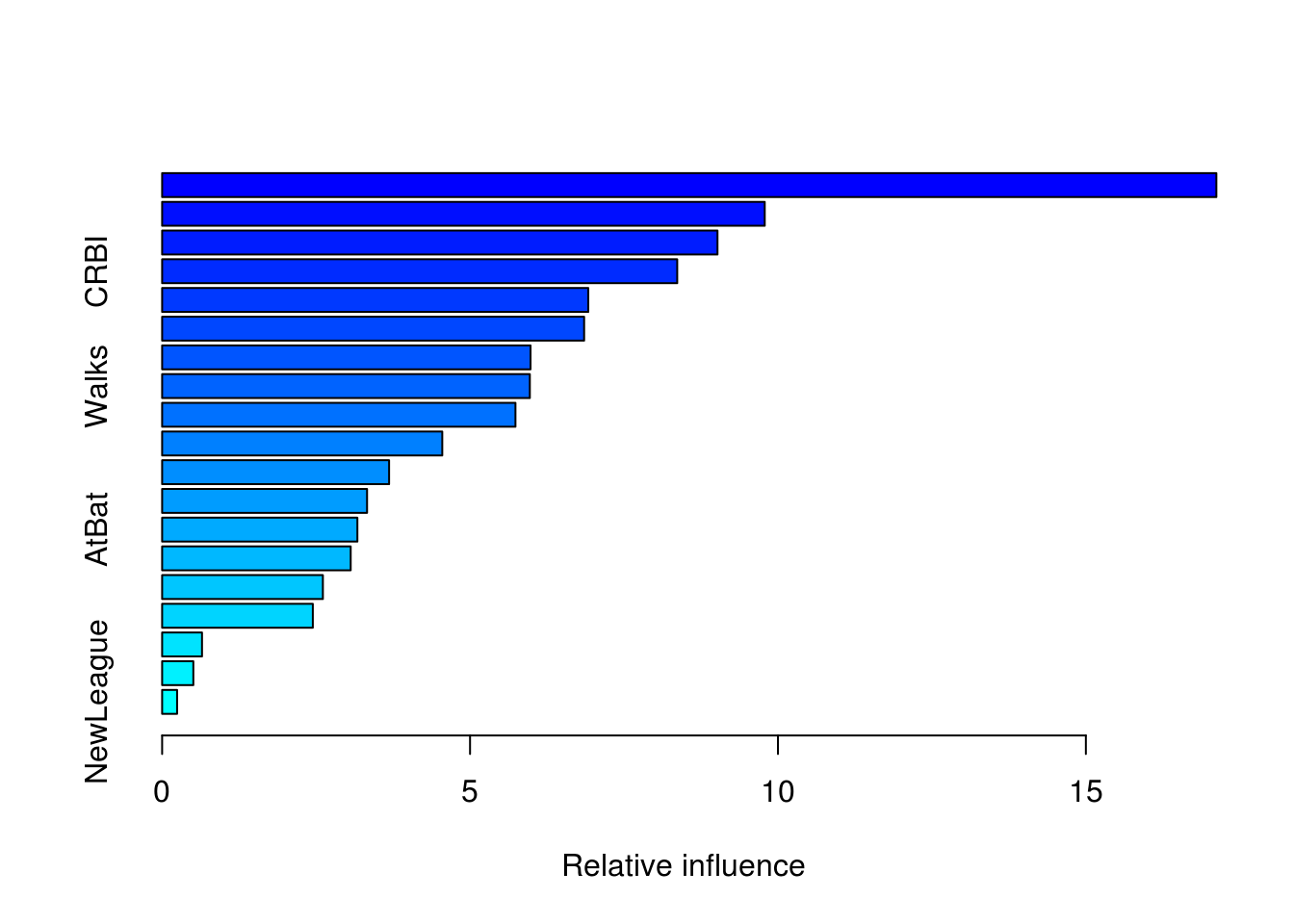

summary(boost_model)

var rel.inf

CAtBat CAtBat 17.1188801

CHits CHits 9.7853653

CWalks CWalks 9.0182320

CRBI CRBI 8.3641950

Years Years 6.9200672

PutOuts PutOuts 6.8526315

CRuns CRuns 5.9824324

Walks Walks 5.9709905

CHmRun CHmRun 5.7374204

Hits Hits 4.5490252

RBI RBI 3.6855364

Assists Assists 3.3276611

AtBat AtBat 3.1707344

HmRun HmRun 3.0619600

Errors Errors 2.6103787

Runs Runs 2.4470517

Division Division 0.6477526

League League 0.5066292

NewLeague NewLeague 0.2430562CAtBat, CHits and CWalks are three most important variables in that order.

- Now apply bagging to the training set. What is the test set MSE for this approach?

set.seed(12345)

rf_model <- randomForest(Salary ~ . , data = train_set, ntree = 500, mtry = ncol(train_set)-1)

rf_predictions <- predict(rf_model, test_set)

rf_mse <- calc_mse(test_set$Salary, rf_predictions)

rf_mse[1] 0.2291436Test MSE for bagging is about \(0.2291436\), which is slightly lower than the best test MSE for boosting.